Economist Kostas Melas, in a recent interview for newpaper Epohi (12.11), commented on the Commission´s economic projections for Greece and how factors like the the third review process, primary surplusses, private consumption, unemployement and tourism growth will impact GDP growth. Melas believes that the conclusion of the third review, the reduction of non-serviceable loans, and discussion on debt relief with a more prositive outlook constitute some very favorable factors for the Greek economy. Overall, Melas posits, taking into account Europe’s economic growth and the lenders’ more favorable attitude towards Greek economy, as far as far the European economic climate is concerned, things are looking up.

The European Commission’s economic forecast for the Greece has been recently published. What is the overall image?

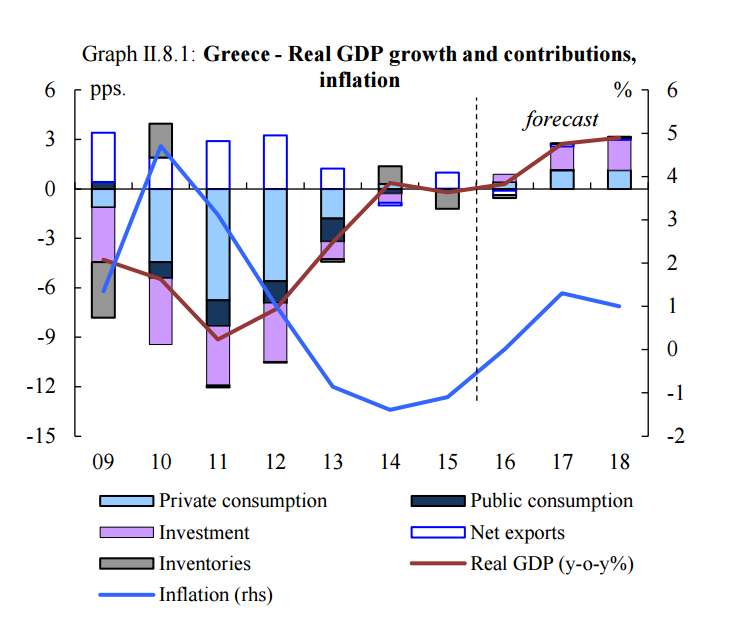

For 2017, Commission estimates a growth rate of 1.6%, which is attributed to the fact that, at least up to the first half of the year, we are seeing a slighter expansion of private consumption and a delay, especially in the second quarter, in investments. The Commission’s previous projection, on March 2017, was for a 2.1% of growth. I think that the projections of the medium-term program 2018-2020 submitted by the Greek government are more correct: 1.8% growth in 2018, private consumption growth of 1.3% and investment growth of 5.9%. Different estimations reflect the different times during which they were made. As we approach the end of each period reviewed and we have more data available, the projections reflect reality more closely. If I made estimation, at this time, I would say that the GDP growth rate for 2017 will be around 1.5% – it could settle at 1.6%, 1.7% or 1.4%.

The question however is, what do these numbers mean for the economy? The primary surplus was set at 1.75%, for 2017 but it will probably reach 2.8%, and the question is how this is linked to GDP growth. They are probably negatively associated, because a higher primary surplus takes resources from away the economy, it reduces demand. It is not the only factor; we also have to consider the extension of the review process and the associated uncertainties. And let’s not forget that private consumption accounts for 70% of GDP. From ELSTAT´s (Hellenic Statistical Authority) data, we are seeing that disposable income fell in 2016, as well as during the first two quarters of 2017.

So are we likely to see a reduction in disposable income for 2017?

Yes, definitely. We will see what happens in 2018 (although reduction will probably continue), but we must not forget that Greece is still undergoing fiscal consolidation. For 2018, as well as for 2019 and 2020, there are still specific fiscal adjustment measures to be taken.

But there will also be countermeasures.

Yes, there will be, but the final balance remains to be seen. There will still be pressures on disposable income. We must also take into account a fundamental parameter: savings. Disposable income is equal to consumption minus savings. Given that now in Greece disposable income decreases at a rate faster than consumption, savings also are decreasing more rapidly. Since 2012, savings have been in negative numbers, and this trend is not slowing down, it decreases at an increasing pace.

Commission´s Autumn 2017 Economic Forecast for Greece (pdf)

Commission´s Autumn 2017 Economic Forecast for Greece (pdf)

With all the available data we have, and based on the fact that economic uncertainty has receded, can we say that the recovery has begun, that there is a certain positive momentum?

The Commission’s estimations are based on how specific factors will evolve. They are anticipating, for example, increased investment. We will see how investments perform in 2017, and if they are on a stable growth path. The second thing to look out for in 2018 is whether we will have an increase in consumption -through the reduction of unemployment- and to what extend. The Commission foresees further reduction in statistical unemployment; it is projected to decline by 1.4% in 2018.

One factor that affects almost all indicators is tourism. At some point, of course, tourism will reach a growth ceiling, but if in 2018 tourism grows as much as it did this year, it will be very important, as this affects both employment and consumption, thus helping GDP growth. On the other hand, I don’t expect the tax burden to be reduced in 2018. If the 2017 growth rate settles at 1.5%-1.6%, then the Commission’s projections for 2.5% in 2018 and 2.5% in 2019 are realistic. But at the same time it is too early to be confident for that, because there are many factors to consider. The economic climate, of course, will be certainly more positive in 2018. The conclusion of the third review, the reduction of non-serviceable loans, and discussion on debt relief with a more positive outlook are some very favorable factors. Taking into account Europe’s economic growth and the lenders’ more favorable attitude towards Greek economy (that is, the does not make things as difficult – the IMF is no longer pressing, because it is, in my view going to abandon the program), I believe that, as far as far the European economic climate is concerned, things are looking up for Greece.

The Commission’s forecasts for budgetary figures are bolder. They surpass the Greek government’s forecasts for both 2018 and 2019. Are they affected by the outperformance of 2016 and 2017, predicted GDP growth, etc.?

If by the end of 2017 we have a surplus of around 2.8%, this will be, indeed, a good basis for 2018. This projection is based on the assumption that the tax collection rate achieved in 2017 will continue due to GDP. It remains to be seen.

Non-serviceable loans are at the center of the debate again. How does this issue evolve?

Both ECB and the Commission want to reduce non-serviceable loans as quickly as possible. This is reflected in Finance Minister’s Euclid Tsakalotos’ recent statements. The perpetuation of this issue is not positive for the banks. It will be very complicated if something goes wrong with stress tests. It is also a crucial factor, as we know, for funding economic activity. The mistake, from the beginning, was adopting a policy for the reduction of public debt but not for private debt as well. Banks tried to make adjustments, but always with their own criteria. Now there is a relative change in how they deal with non-serviceable loans, providing different options to borrowers, such as paying whatever part of the debt they can and “freezing” the rest. This is an attempt to make more realistic adjustments.

I.L.